Case SPA R5: Changing Eligibility Criteria? Why Traditional SDLC Breaks and How Software Platform Anatomy Ensures Stability

- Krish Ayyar

- Mar 28, 2025

- 4 min read

Updated: Oct 10, 2025

Category: Rules & Motivations in Flux

Series: Rethinking Requirements: How the ICMG Enterprise Anatomy Model Makes Systems Change-Ready

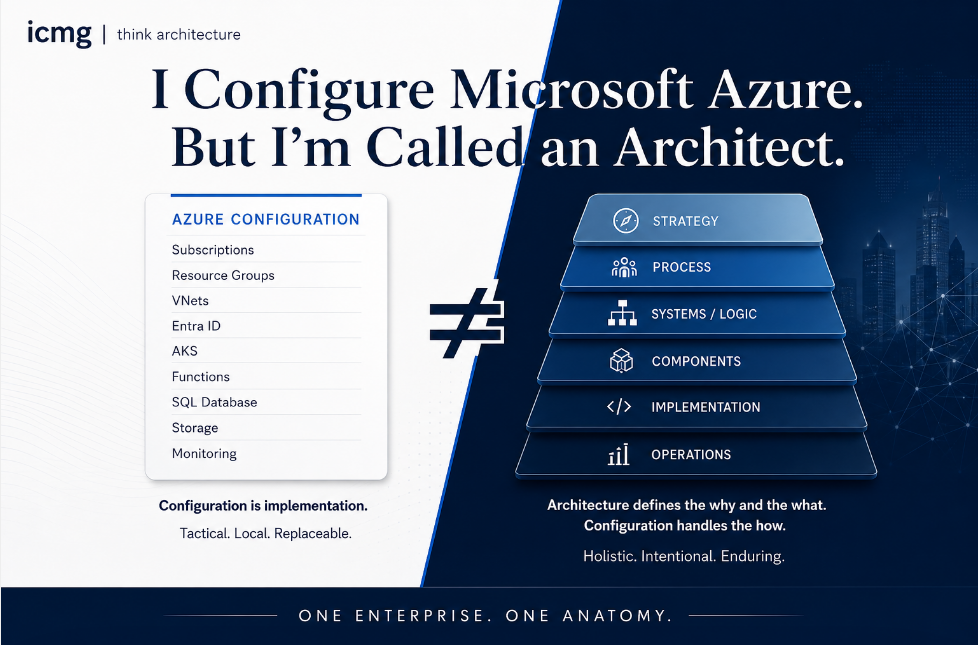

Perspectives Covered: Strategy, Business Process, System, Component Specification, Implementation, Operations

Key Variables Impacted: Rule, Data, Event, UI, Function, Network

In this post, we explore a requirement change scenario driven by a shift in credit risk policy—an example of a Rule/Motivation change. We examine how such a change impacts the lending architecture and how the ICMG Enterprise Anatomy Model (Project Edition) enables precise, coordinated responses across the architectural perspectives and variables involved.

Perspectives covered: Strategy, Business Process, System, Component Specification, Implementation, Operations

Key variables impacted: Rule, Data, UI/Access Channel, Event

The Challenge of Frequent Requirement Changes

Retail lending is a dynamic space. Loan eligibility criteria evolve constantly due to shifts in credit risk appetite, regulatory directions, and business strategy.

Consider a typical requirement change:The credit policy team increases the minimum credit score for loan eligibility from 650 to 700.

While the change may seem simple, in most lending systems it leads to significant disruption:

Developers must modify code across multiple systems

UI and backend display inconsistent eligibility decisions

Pre-approved customers are incorrectly accepted or rejected

Testing becomes reactive and manual

Business teams lose confidence in delivery

These problems arise because most teams react at the implementation level without understanding the system’s architectural anatomy. The ICMG Enterprise Anatomy Model (Project Edition) addresses this challenge through a structured, multi-perspective, variable-driven approach.

Why Conventional SDLC Approaches Fail

What goes wrong:

Credit score rules are hardcoded across backend services, APIs, and decision engines

Customer portals display outdated or inconsistent messaging

Loan officers manually override system behavior

Compliance reports reflect incorrect approval decisions

The root cause:

Want to read more?

Subscribe to architecturerating.com to keep reading this exclusive post.